Let’s start with the uncomfortable part.

Anthropic just published research ranking the professions most exposed to AI. Market research analysts and marketing specialists came in at 65% task exposure. Sales reps: 63%. These aren’t hypothetical projections — they’re based on actual Claude usage logs pulled from real workplaces. Not what AI could theoretically do. What it’s already doing.

If you run a services business — an agency, a consultancy, a boutique firm selling expertise by the hour — that number should make you uncomfortable. Because most of what you sell sits squarely in that window. And unlike physical jobs, there’s no “AI can’t be in the room” defense. Your room is a browser tab. AI is already in it.

The Barrier Problem

Here’s what nobody in the services world wants to say out loud: you have no moat.

Five years ago, running good digital campaigns took real expertise. Media buying, creative strategy, audience segmentation — skills that took time to develop, and clients paid a premium for. The barrier to entry was knowledge.

That barrier is gone.

Any founder with a $50/month subscription and a Sunday afternoon can now produce campaign strategy, ad copy, audience briefs, and competitive analysis that would have cost $20K at an agency two years ago. The output isn’t always great. But it’s good enough to make your prospect ask why they’re paying you.

If all you do is branding better than everybody else, you are in trouble. Because “better” is getting harder to prove when the client can generate five brand directions before lunch — and one of them is actually pretty good.

The Survivors Are Builders, Not Executors

Anthropic CEO Dario Amodei has said AI could disrupt half of entry-level white-collar work. He’s not wrong. But the displacement isn’t random — it’s hitting the work that’s generic first. The execution. The production. The stuff any LLM can crank out at 2am for free.

What AI can’t replace is the person who had the original thought.

The survivors in this industry are going to be the creators, the product managers, and the builders. People with a genuine point of view on how to reach an audience — not just the ability to produce content about it. People who can direct AI, not just operate it. The difference between a film director and a camera is not going to close, no matter how good the camera gets.

If you’ve spent years developing a real approach — a way of recognizing buyer behavior, sequencing a message, building an audience model that actually converts — that’s yours. That’s not something any LLM can generate from scratch.

What the LLM can do is scale it.

But here’s the thing: you have to be able to prove it.

Not describe it. Not put it in a case study PDF. Prove it. Show that your method consistently outperforms what the model produces on its own. Show the lift. Show the conversion delta. Show the before and after. Show it more than once.

That proof is your moat. And you should be screaming it from the rooftops.

One way to validate it is to encode your methodology into a system — train it on your own data, run it against a control, and let the numbers speak. That’s one path. But the proof itself is what matters, however you get there. The format is secondary. The evidence is everything.

Because right now, every services firm on earth is claiming they “use AI strategically.” That phrase means nothing. What cuts through is: here’s what we do, here’s what the model does alone, and here’s the gap. If you can show that gap consistently, across clients, you have something nobody can commoditize.

Your Data Is the Differentiator. Protect It Like One.

There are two kinds of operators building on AI right now.

The first is using the same tools everybody else has access to. Open source models, public datasets, off-the-shelf platforms. Nothing wrong with that — it’s fast, it’s cheap, and it gets you started. But it’s not defensible. If anyone can replicate your stack on a weekend, your stack isn’t a moat.

The second kind is sitting on something nobody else has: their own data.

Campaign performance across years of real client spend. Audience response patterns that only exist because they ran the tests. Behavioral signals trained on specific verticals. That data isn’t available in any public dataset. It can’t be scraped. It can’t be prompted into existence. And an LLM — no matter how capable — cannot replicate what you know from having actually done the work.

That’s privately provable data. And it is IP.

The distinction matters at exit. A firm selling services gets valued on EBITDA. A firm that can show proprietary data assets — validated audience intelligence, documented lift against control, a methodology that demonstrably outperforms the generic model — starts a very different conversation with a buyer. You’re not selling a book of business anymore. You’re selling something that can’t be rebuilt from scratch.

The practical move: start treating your performance data like a product asset right now. Document your methodology. Track your lift. Build the proof set. You don’t need a machine learning team to start — you need a discipline around capturing what works and why, so when the time comes to encode it or sell it, the evidence is already there.

Open source tools are fine for execution. Privately provable data is what you sell.

A Word on the AI Graveyard

Before we get to the math, let’s clear something up.

There is absolutely a graveyard of “AI products” that were never real. Thinly veiled ChatGPT wrappers with a logo slapped on them. Prompt libraries dressed up as platforms. Generic automation tools with “powered by AI” in the footer. Most of them are already dead or dying, and they deserve to be.

That’s not what this is about.

This is for the operators who already have something real. A proprietary data set. A structure. A process. A repeatable system that produces measurably better outcomes than what anyone else is doing. Something you’ve run on real clients, with real budgets, and gotten real results. Something you could — and in some cases should — patent.

If that’s you, keep reading. If you’re looking for a shortcut, this isn’t it.

The Math That Changes Everything

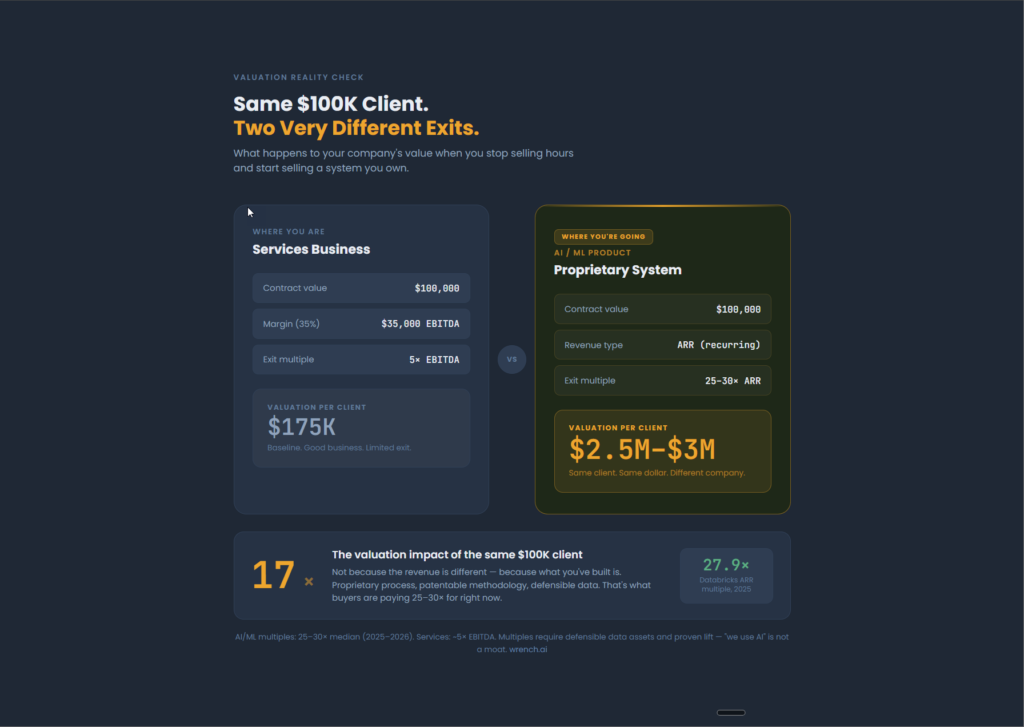

Most services businesses exit at roughly 5x EBITDA. That’s the game. You build something, you margin it well, and someday you sell it at a multiple of what you kept.

Here’s what it looks like in practice:

Services math:

- $100K contract at 35% margin = $35K EBITDA

- At 5x EBITDA → $175K in valuation per client

Now encode that methodology. Protect it. Patent the process where it qualifies. Turn the repeatable system into a product with proprietary data behind it.

AI/ML product math:

- $100K ARR at 25–30x (current AI company median) → $2.5M–$3M in valuation

- That’s 15–17x the valuation impact of the same contract dollar

- Companies with defensible proprietary data assets are commanding these multiples right now

That’s not a rounding error. That’s a different company.

Databricks is the clearest real-world proof — proprietary data infrastructure and ML pipelines took it from a $62B valuation in late 2024 to $134B by 2025, at a 27.9x ARR multiple. Buyers pay that premium for the same reason your methodology has value: it can’t be rebuilt from scratch.

One honest caveat: multiples compress fast without proof. “We use AI” is worthless. No one’s going to buy based off empty promises. They will check. They will look behind the curtain at how much revenue, recurring revenue, repeated revenue, churn, documented lift, repeatable results, and defensible data assets are what hold the multiple. Which is exactly what the previous section is about. The less you have, the less your valuation will be impacted.

What It Actually Takes

This is where most owners check out. So let’s be direct about the cost.

You’ll spend roughly $100K to build, test, and pilot something real. You’ll run unpaid or deeply discounted early clients to prove it works. You will not be profitable on client one in month one. Your P&L will look worse before it looks better, and your CFO will have opinions about it.

You also have to get close enough to a software business model to matter — which means thinking about customer acquisition cost differently, accepting longer payback periods, and funding the gap between build and commercial scale.

This is not a weekend project. It takes a shift in mindset, it requires moving on from needing to be profitable in the first month mindset. It may require team change management and will transform how you propose and vet clients over a year or more. And yes, you have to deal with the general bullshit of building a product, vs a service.

But here’s what’s on the other side of that: clients who built targeting methods so distinct they patented them. One-to-one personalization that doesn’t require a human in the loop to execute. One client saw 4,300% ROI on their spend. That’s not a typo, and it’s not an outlier — it’s what happens when a system that actually works gets to scale.

The Choice

The services providers that figure this out in the next two years will be worth materially more than the ones that don’t.

The ones that don’t will be competing on price against a $50/month subscription.

If you’ve built a system, you can productize it. If you can productize it, you can scale it. If you can scale it, you can sell it — at a multiple that reflects what it actually is.

That’s the exit. That’s the valuation story. That’s how you stop surviving the AI era and start building something worth selling.